May 12, 2024 | 714-336-0394 | Scot@CampbellRealtors.com | Broker of Record – Coldwell Banker-Campbell Realtors

As one of the very few practicing real estate professionals in California who has worked through all the Agency changes in California Residential Real Estate Transactions over the last 40 years, I can effectively explain where the real estate industry has been with the rules of agency, and where it is today given the recent NAR Settlement.

In 1982, I started working in my father’s real estate office (while I was still in high school). A licensed California Real Estate Broker since 1957, E.J. Campbell is the founder of our brokerage. At that time, the standard real estate practice in California when selling a home was to hire a Seller’s Agent. That brokerage was known as the “Listing Agent”, and customarily a portion of the commission was “offered” through the Realtor MLS to a “Cooperating Brokerage” who was deemed a “Sub-Agent” of the Seller’s Listing Agent.

The fiduciary duty of the Seller’s Listing Agent and Cooperating Brokerage (Sub-Agent) was entirely to the Seller of the home. This would be just as you would expect at a car dealership… everyone you speak with is trying to sell the vehicle for the maximum profit for the dealership. There is no one looking out for the interests of the “car Buyer” at the automobile dealership, and prior to 1984 there was no one looking out for the interests of the home Buyer. The concept of “Buyer Beware” ruled the day.

Easton V. Strassburger (Buyer Agency Begins)

In 1984, there was a revolution in the rules of real estate agency. The practice of “Buyer Agency” was introduced following the Easton V. Strassburger case. It became best practices and Real Estate Law for real estate agents to be either: The Buyer’s Exclusive Agent, the Seller’s Exclusive Agent, or a Dual Agent Representing Both Buyer & Seller. However, to the dissatisfaction of many home Sellers, the law and existing practice in the industry provided that the Seller pay the commission for both the Seller’s Agent and the Buyer’s Agent.

As much as some home Sellers were dissatisfied with the concept, the policy benefited the Sellers; here are the reasons why:

VA Buyers have zero money to pay a Buyer Agent commission. In fact, the Veterans Administration does not permit them to pay a commission. If the Seller does not pay the commission for VA transactions, these Buyers leave the pool of potential home purchasers.

FHA Buyers have zero money to pay a Buyer Agent commission. They are scraping up 3.5% to put down on a home, it could take months or years to save enough money to pay a Buyer Agent commission. If the Seller does not pay the commission for FHA transactions, these Buyers may never join the pool of potential home purchasers.

Most Buyers are trying to reach down payment thresholds to lower their payment and qualify for a higher loan: 5%, 10%, 15%, and 20%. Each time one of these levels is reached, there is a savings in the cost of borrowing with either a lower rate/points or the elimination of Private Mortgage Insurance (at 20% down). The higher the Buyer’s down payment as a percentage of the purchase price, the easier it is for the Buyer to qualify for the loan.

Seller paid Buyer Agent commissions allow the Buyer’s down payment to be larger. For example: with 20% down, an increase in the Buyer’s down payment of $20,000 allows the Buyer to finance an additional $100,000. The Sellers benefit from the Buyer having more money to put down, thus pay more for the home. Example: If the Seller pays the $20,000 commission, the Buyer can pay $100,000 more for the home.

Once these facts were explained to the “dissatisfied” home Sellers (who were upset that they were paying a commission to a Buyer’s Agent), the Sellers quickly agreed to the practice. They did this not do this because they were “nice”, it was done because paying the Buyer Agent commission was in the best interest of home Sellers.

Burnett v. National Association of Realtors (Jury Decides Changes are Needed)

Fast forward to 2023. A law firm found a new group of “dissatisfied home Sellers” and filed a lawsuit against the National Association of Realtors which alleged that these Sellers had been defrauded. The contention was they were forced to pay a Buyer Agent commission and Realtors were preventing negotiations on commission rates.

The case was filed in the State of Missouri, Burnett v. National Association of Realtors (“NAR”), et al. In October 2023, it was reported that a jury (none of whom were home owners) found in favor of the disgruntled Sellers. The Missouri Jury was successfully convinced that Home Sellers felt compelled (or were explicitly told) to pay a commission to Buyer’s Agents.

The jury felt that it was implied (or stated) that Buyer Agents might refuse to show their property (if a lower commission was offered), fostering fear that their home would not sell.

They felt it was unreasonable that the commission remained the same even if the Buyer independently found the home, attended an open house without an agent, conducted an analysis of comparable properties using publicly available data, and only contacted the Buyer’s Agent for assistance with the offer paperwork.

Compounding the issue, the real estate industry enacted arguably self-serving rules (MLS Rule 9.7 and NAR Standard of Practice 1616) prohibiting licensed real estate agents from assisting Sellers in negotiating lower Buyer’s Agent commission as part of the offer/counter-offer process.

A Landmark Settlement (NAR Agrees to Rule Changes)

On March 15, 2024 the National Association of Realtors entered into a settlement in the Burnett V. NAR case which as of today’s date is awaiting approval by the court.

As part of the settlement, NAR agreed to the following MLS rule changes which will become effective in Mid-August 2024:

Agents are required to sign a written Buyer Representation Agreement with their Buyer Clients wherein compensation to be paid by the Buyer is specified.

Seller paid Buyer commissions will no longer be published in the Realtor MLS.

Furthermore, NAR has issued specific guidance that agents should always tell clients:

“Compensation arrangements (including commissions) are, and have always been, negotiable and set between a broker and their respective client… “

“Listing brokers in consultation and agreement with their Seller clients decide how much compensation to offer to serve the Seller’s best interest, and it can be $0, $1, or any other amount. NAR rules do not specify an amount for commissions. This is solely a matter that’s negotiated between brokers and their clients.”

Effect of the settlement on Coldwell Banker – Campbell Realtors policy & practices

A New Era in real estate is beginning soon. The marketing success and closing of a home sale for top dollar in this New Era will be determined by the skillset of the Listing Agent. These are the objectives we will maximize:

The number of qualified Buyer online views, in-person viewings of the property, and Buyer Agent Showings

The number of offers submitted by qualified Buyers (either through Listing Agent or cooperating Buyer Agent)

The sale price, optimal terms, and net proceeds desired by the Seller

Our policies and practices as the Listing Agent will remain aligned with the home Sellers who have hired us to market their properties. Accordingly, we invite Sellers to read our New Marketing Plan to Sell your Home which is now being completely revised for the New Era in real estate which begins in Mid-August 2024.

In consultation with California Assn of Realtors attorneys, we have found elegant solutions for: VA, FHA, and Buyers with down payment threshold issues.

By Scot D. Campbell, Broker of Record ~ Coldwell Banker-Campbell Realtors, Huntington Beach, CA

In response to the Sitzer/Burnett v. National Association of REALTORS® (“NAR”) lawsuit, NAR announced changes to the Realtor MLS rules.

The changes reflect the most significant modification of the rules of agency since the practice of Buyer Agency was introduced following the Easton V. Strassburger case in 1984.

The changes to the Multiple Listing System were announced on March 15, 2024 and the rules will become effective in July 2024:

1) Agents are required to sign a written Buyer Representation Agreement with their Buyer Clients wherein compensation to be paid by the buyer is specified.

2) Seller paid buyer commissions will no longer be published in the Realtor MLS. Instead, the listing agent will publish a dollar amount or percentage that the seller is offering to credit the buyer through escrow for the payment of closing costs including the Buyer Agent commission.

The NAR announcement has left many Homebuyers with questions and concerns:

Q: Will buyer representation agreements become mandatory under California law?

A: We don’t know whether there will be future proposed legislation that requires California licensees to use Buyer Representation Agreements; however, it is clear that the industry is moving toward mandatory agreements between Buyers and their Agents.

Coldwell Banker-Campbell Realtors uses a one-page Simple Buyer Representation Agreement along with the C.A.R. Standard Form BRBC (which specifies that the seller credit money from escrow to pay the Buyer Agent commission).

Q: What if a buyer doesn’t have enough money to pay for a Buyer Agent commission?

A: The C.A.R. Standard Form BRBC can be included with any offer a buyer wishes to make on either listed or unlisted properties. In essence, a credit to the buyer’s closing costs from the seller pays the Buyer Agent commission in the amount previously negotiated between the Buyer and the Buyer Agent in the Buyer Representation Agreement.

Q: Will this change how homes are bought and sold in California?

A: The answer is absolutely “Yes”. Buyers will formally “hire” a Buyer Agent and the agent compensation will be agreed in writing before commencing the process of locating a home to purchase.

Q: Can a seller choose to offer “No Commission” to the Buyer’s Agent?

A: The answer is absolutely “Yes”. But, practically this has been the case for many years in our area. The California Regional Multiple Listing Service has maintained rules which allow an offer of compensation to the Buyer’s Agent of just “One Dollar”. Yet, sellers have very rarely offered a $1 commission because “no commission” was found not to be a sound marketing strategy for home sellers who wanted to generate as many showings and offers as possible.

Q: Can a seller choose to offer No Credit to the Buyer’s closing costs when an offer is submitted.

A: The answer is absolutely “Yes”. But, the new NAR rules call for an announcement in the MLS for each listing indicating how much of a credit the Seller is offering to the Buyer for closing costs which the Buyer can use to pay the commission.

Just as Sellers found in the past that offering a $1 commission not a sound marketing strategy generating lots of showings & offers, it is likely that Sellers will discover the same is true if they offer No Credit to the Buyer’s Closing Costs (for payment of the commission).

Q: If the seller is offering a credit in the Realtor MLS that is less buyer wants, can the Residential Purchase Agreement “offer” include a Credit Request which is greater than what was published in the MLS?

A: The answer is absolutely “Yes”. This is exactly what the C.A.R. Standard Form BRBC was designed to do for Buyers.

Q: How much of a commission should the Buyer agree to pay the Buyer’s Agent in the written Buyer Representation Agreement?

A: Commissions are negotiable by law. The commission you elect to pay your Buyer’s Agent is up for negotiation.

A very responsive agent working for a reputable brokerage with a brick & mortar office who provides you with Full Service in locating the property, negotiating the sale, helping with inspections & the Request for Repair, following up on escrow, making sure the Seller follows the terms of the Residential Purchase Agreement, and countless other details is worth much more than a Buyer Agent who offers little or no help other than writing the offer… and happens to have very poor negotiating & follow-up skills.

Like anything else, you get what you pay for… and buying a home is generally the biggest financial decision you will make in your lifetime. Good advice is very valuable, and a hard-working agent can make the difference between a good transaction and a regrettable one.

Ultimately you will decide the Buyer Agent commission offered to your Coldwell Banker-Campbell Realtors agent, and your agent will do their utmost to negotiate a credit offered by the Seller in an amount which covers the commission.

At the end of the day, the Seller has put their property on the market to get it sold… not to quibble about how much the Buyer’s Agent is going to be paid.

From reading the headlines in the media, you might think that most sellers that contacted me asked the questions: “Does this mean I do not have to pay a commission to get my home sold?”

Perhaps you think Sellers are thrilled about the NAR Announcement. In fact, they are not happy, they are worried. The question I received from Seller clients since the ruling was this: “How am I going to get my home sold if I can no longer offer a commission to Buyer Agents to bring buyers to purchase my home?”.

Sellers understand that Buyer Agents perform many important tasks in real estate transactions… starting with having the “trust” of the Buyer which was built during the interview process or because the agent has already done transactions with the buyer, their family, or friends in the past.

Sellers rely on Buyer Agents to bring prospective buyers to see their home, explain why the home is a good one to purchase, and demonstrate the value of the home using neighborhood sales comparables.

The truly savvy Sellers understand that without Buyer Agent Representation, many… perhaps most, Buyers would never write a market price offer on their home.

Certainly, the law of unintended consequences is now in effect. It will take a little time for the residential real estate industry to settle in on a new set of standard practices.

At Coldwell Banker – Campbell Realtors the management team has over 50 years of experience. We are determined that the recent NAR Announcement and rule implementation shall not take the Dream of Home Ownership away from any of our clients.

Our greatest concern is that a future interpretation of the rule changes will negatively affect buyers using FHA & VA financing. Understand that we will be advocating for all of our low down payment clients in our discussions with the C.A.R. attorneys.

Rest assured, we are in consultation with our attorney and top attorneys at C.A.R.

It is my goal as the Broker of Record for Coldwell Banker-Campbell Realtors to minimize any negative aspects for home sellers which may result due to the rule changes announced by NAR.

I am available to speak with you on the telephone or we can meet in person at our oceanfront office to answer all of your questions via phone, text, or email: 714-336-0394 ~ Scot@Campbellrealtors.com

NOTE: The information contained in this Q&A is from the most accurate data sources as of March 17, 2024. It is possible and likely that bulletins & rulings from the California Department of Real Estate, Federal Department of Justice, and Federal Judges may clarify or change the landscape. We will issue further guidance as new information becomes available. We welcome your inquiries as to any changes, and it is recommended that you verify all aspects contained above as you move forward with your real estate transaction.

By Scot D. Campbell, Broker of Record ~ Coldwell Banker-Campbell Realtors, Huntington Beach, CA

The changes reflect the most significant modification of the rules of agency since the practice of Buyer Agency was introduced following the Easton V. Strassburger case in 1984.

The changes to the Multiple Listing Service were announced on March 15, 2024 and the rules will become effective in July 2024:

1) Agents are required to sign a written Buyer Representation Agreement with their Buyer Clients wherein compensation to be paid by the buyer is specified.

2) Seller paid buyer commissions will no longer be published in the Realtor MLS. Instead, the listing agent will publish a dollar amount or percentage that the seller is offering to credit the buyer through escrow for the payment of closing costs including the Buyer Agent commission.

The NAR announcement has left many Home Sellers with questions and concerns:

Q: Will buyer representation agreements become mandatory under California law?

A: We don’t know whether there will be future proposed legislation that requires California licensees to use buyer representation agreements; however, it may become a practical necessity in order for Buyer Agents to get paid a commission.

Coldwell Banker-Campbell Realtors uses a one page Simple Buyer Representation Agreement along with the C.A.R. Standard Form BRBC (which specifies that the seller credit money from escrow to pay the Buyer Agent commission).

The Standard Form CBC (which specifies seller paid Buyer Agent commission might be used as an alternative especially for VA & FHA transactions… more on this later in this Q&A)

Q: What if a buyer doesn’t have enough money to pay for a buyer’s agent?

A: The C.A.R. Standard Form BRBC can be included with any offer a buyer wishes to make on either listed or unlisted properties. In essence, a credit to the buyer’s closing costs from the seller pays the Buyer Agent commission in the amount previously negotiated between the Buyer and the Buyer Agent in the Buyer Representation Agreement.

Q: Will this change how homes are bought and sold in California?

A: The answer is absolutely “Yes”. In many cases, Buyers will formally “hire” a Buyer Agent and the agent compensation will be agreed in writing before commencing the process of locating a home to purchase.

Q: Can a seller choose to offer “No Commission” to the Buyer’s Agent?

A: The answer is absolutely “Yes”. But, practically this has been the case for many years in our area. The California Regional Multiple Listing Service has maintained rules which allow an offer of compensation to the Buyer’s Agent of just “One Dollar”. Yet, sellers have very rarely offered a $1 commission because “little or no commission” was found NOT to be a sound marketing strategy for home sellers who wanted to generate as many showings and offers as possible.

Q: Can a seller choose to offer No Credit to the Buyer’s closing costs when an offer is submitted.

A: The answer is absolutely “Yes”. But, your Net Proceeds should be your primary consideration. The more money the buyer has available to use for the down payment, the higher the loan they can qualify for, and thus the more they can pay for your home. If you choose to not offer a credit for the Buyer to use to pay the Buyer’s Agent commission, you are in effect lowering the purchasing power of the buyer… which is not in your interest as a home seller. With no credit offered to pay the commission, some buyers may choose not to see your home.

Q: Without a clear offer of compensation from the seller or published credit amount, is it likely that some agents will make “less effort” to sell my home?

A: The answer is an absolute “Yes” for Buyer Agents representing VA Loan Buyers (if they feel there is no way to close the transaction and get paid). Buyers using VA financing are not allowed to pay any commission to the Buyer’s Agent. And, many FHA Buyers simply do not have the funds to pay a Buyer Agent commission. This is a very legitimate concern for home sellers and has been the subject of several calls I received today.

We are working to get clear guidance from our attorney now. Although it may not be allowed by NAR rules for the seller to offer compensation to the Buyer Agent through the Realtor MLS, it appears that a separately published written offer by the Seller to compensate the Buyer’s Agent is allowed by law (and common sense). Certainly, a seller who wishes to pay a Buyer Agent (legally an independent contractor) for their services should be allowed to do so for VA, FHA, and any other transaction for that matter.

Q: In order to better motivate agents who represent buyers to show & sell my home, is there another way that a seller can publish an offer of compensation to the Buyer’s Agent once the new NAR rules go into effect?

A: The answer is most certainly “Yes”. A simple blog post on our brokerage website could be a very effective mechanism for publishing the seller’s written pledge to pay the Buyer Agent commission.

When asked by a Buyer Agent about commission, the agent could simply refer them to the published blog post which will have the commission document. The California Association of Realtors already has a form for this purpose, and it can be added as an addendum to the Residential Purchase Agreement.

Certainly, the Buyer Agents who work with VA, FHA, and other low downpayment buyers will be comforted & incentivized by the fact that know they will be paid a commission at close of escrow for a job well done (even if lending rules or available buyer funds do not allow them to get paid a commission by the buyer).

Q: If I offer to pay a Buyer Agent commission and the Buyer demands the majority of the commission be credited to them in escrow, I am concerned I will not get the good service I am paying for… How can I be certain that the Buyer’s Agent is going to get all the commission I paid through escrow?

A: We are verifying this with our attorney. For now, we believe the answer is “Yes”. The blog post that contained the offer to pay the Buyer Agent commission could be conditional on all funds being paid to the Buyer Agent brokerage.

Q: If a Buyer and Buyer’s Agent have entered into a Representation Agreement, what is the mechanism for the Buyer Agent Commission to be paid?

A: The California Association of Realtors has already created a form for this purpose. The form is an addendum to the residential purchase agreement, and it indicates the amount or percentage of the purchase price that the seller will CREDIT to the Buyer through escrow. The Buyer Agent is then compensated by the Buyer through escrow as per the terms of their signed Buyer Representation Agreement.

Q: Is there a way that sellers can publish a CREDIT to the Buyer through escrow so that the Buyer can pay the Buyer Agent’s commission once the MLS system no longer publishes the commission payable to the Buyer’s Agent?

A: Yes, it may be possible for us as your listing agent to publish a blog post which includes the buyer credit addendum already filled out. The form would indicate the amount of the credit you are willing to pay at close of escrow. When asked by a Buyer’s Agent about the amount of the credit you are willing to pay, I could simply refer Buyer Agents to the blog post which would have a downloadable document they can add to the Residential Purchase Agreement. The Buyer’s Agent is going to be keen to learn whether the credit is sufficient to pay the agreed commission in the Buyer Representation Agreement because the buyer is certain to ask.

Q: How large of a commission should be offered to the Buyer’s Agent (if no Buyer Representation Agreement has been signed or as the seller you wish to dictate how much the Buyer Agent is paid)?

A: Commissions are negotiable by law. Just as we have been doing since before yesterday’s NAR announcement, our Seller Clients decide how much commission should be offered to the Buyer’s Agent.

The amount you choose to offer affects your net proceeds… and it also affects the actions of the Buyer Agents (who voluntarily spend time trying to procure a purchaser for your home). So, the amount offered should be consistent with your goals for your net proceeds and at the same time be part of the overall marketing strategy for the property which seeks to get as many buyers to the home as possible to procure multiple offers.

Q: How large of a credit to the Buyer’s Closing Costs should be offered in the addendum (if the Buyer has signed a Representation Agreement with their Buyer Agent).

A: Just as Commissions are negotiable by law, the credit you elect to offer the Buyer for Closing Costs is negotiable. The amount you choose to offer affects your net proceeds, and this decision also affects the actions of the Buyer Agents who spend their time trying to procure someone to purchase your home. Finally, the credit amount may also determine the maximum amount buyers can afford to pay for your home. The amount offered should balance all of these concerns.

Ultimately the Buyer Agent commission or credit amount offered should be carefully considered and consistent with your goals for both net proceeds… and as a successful component of the overall marketing strategy. For our seller clients, it is always our intent to maximize:

1) The number of qualified buyers coming to see the property

2) The number of offers submitted by buyers

3) The sale price & net proceeds (based on the seller’s desired terms)

Certainly, the law of unintended consequences is now in effect. It will take a little time for the residential real estate industry to find a new set of standard practices.

We are in consultation with our attorney and top attorneys at C.A.R.

It is my goal as the Broker of Record for Coldwell Banker-Campbell Realtors to minimize any negative aspects for home sellers which may result due to the rule changes announced by NAR.

I am available to speak with you on the telephone or we can meet in person at our oceanfront office to answer all of your questions via phone, text, or email: 714-336-0394 ~ Scot@Campbellrealtors.com

NOTE: The information contained in this Q&A is from the most accurate data sources as of March 17, 2024. It is possible and likely that bulletins & rulings from the California Department of Real Estate, Federal Department of Justice, and Federal Judges may clarify or change the landscape. We will issue further guidance as new information becomes available. We welcome your inquiries as to any changes, and it is recommended that you verify all aspects contained above as you move forward with your real estate transaction.

Come to our office via 18th Street (driving on 18th Street toward PCH from Walnut Avenue), or from Pacific Coast Highway (driving from the 17th Street), turn right on 18th Street. There may be a line of cars lined up on PCH.

When you arrive to the parking lot, follow the line of vehicles. Your boxes will be unloaded from the back of your car and placed into a rolling bin which will be shredded on site by the Pro-Shred Security truck.

It is best to arrive early… in some years we have filled up the trucks to capacity before the end of the event.

You are certainly welcome to tell your friends, family, and co-workers about the event.

Our goal is to help as many people in the community as we can with the secure shredding of their old financial and medical documents.

Oh by the way… if you know anyone thinking of Buying or Selling real estate, I am here to help.

My observations of Huntington Beach real estate market conditions allow me to provide valuable insights to home buyers & sellers.

If you have a minute, allow me to point out the trends and conditions that drove the real estate market over the last 10 years.

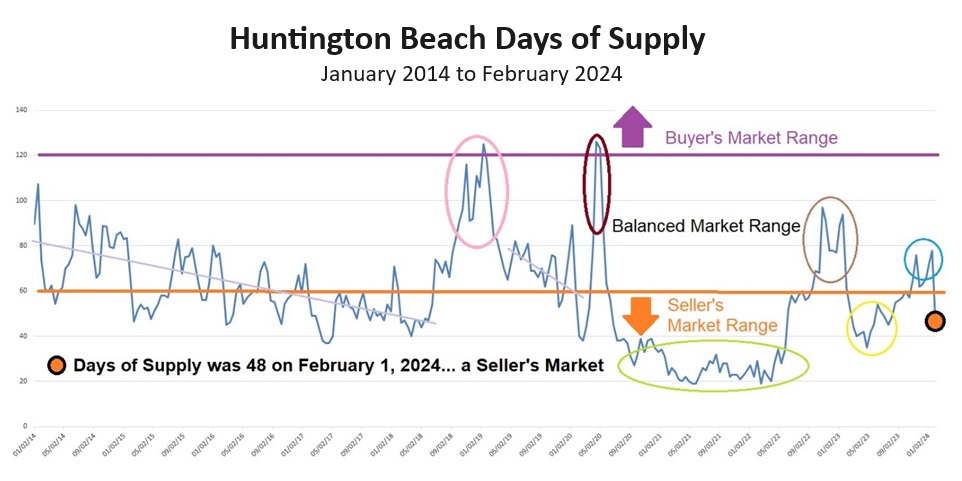

Days of Supply is defined as the number of days it would take to sell every home presently on the market at the current rate of sales if no new listings came on the market.

It is the metric which provides the best indication of the overall strength of the real estate market, and I have been tracking it closely for many years.

When Days of Supply is “high”, this means that there are a lot of homes on the market relative to the number of homes selling. We consider a level 120 or greater to be a Strong Buyer’s Market.

When Days of Supply is “low”, this means that there are few homes on the market relative to the number of homes selling. We consider a level of 60 or below to be a Strong Seller’s Market.

Take a look at the below graph. I will walk you through market conditions from 2014 to February 2024.

From 2014 through 2018, the market saw a general strengthening as shown by the light purple regression line. The mean level of Days of Supply fell from 80 (Balanced Market) to 50 (Strong Seller’s Market).

The pink oval shows the Days of Supply peaked at 125 (Buyer’s Market) on January 10, 2019 due to a combination of the elimination of the Mortgage Interest Tax Deduction and an increase in mortgage rates to 4.94% in November 2018.

From February 2019 to February 2020 (just prior to CV-19) the light purple regression line shows market conditions improved rapidly with the level of Days of Supply falling to just 40 (Strong Seller’s Market).

At the inception of the CV-19 shut down, the dark red oval shows Days of Supply spiked at 126; however, as interest rates fell and consumers looked to relocate during the pandemic, the Days of Supply plummeted back to 40 (Strong Seller’s Market).

From July 2020 to May 2022 the green oval shows the Days of Supply hovered between 18 and 38… this was the strongest seller’s market on record. Most likely the strongest imbalance between supply and demand which will ever be seen in our lifetimes. Huntington Beach was seen as an ideal remote work location, interest rates were low, and government stimulus programs put billions of dollars into the economy. Just about every home had multiple offers, and many sold for thousands of dollars above the asking price.

Then… in the Spring of 2022 mortgage interest rates went up over two percent! From June 2022 to February 2023, the dark green oval shows the Days of Supply into the 60 to 97 range. It was a Buyer’s Market in the $2 Million+ price segments and balanced market conditions down into the $800,000 to $1,200,000 range. Mortgage rates rose steadily spiking to 7.08% in November of 2022, and then dropped to 6.13% by February 2023.

These low rates in the Spring of 2023, allowed the Days of Supply to fall back to the 35 to 55 range (Strong Seller’s Market) range March and August, see Yellow Circle.

Then mortgage rates began rising once again and peaked just over 8% in October 2023. The aqua blue circle shows the Days of Supply responded as expected reaching 78 on January 18, 2024.

Favorable inflation reports and a pause in the increase of interest rates by the Federal Reserve in November 2023 resulted in mortgage rates plunging over 150 basis points. The result was an increase in buyer purchasing power and activity. Predictably, the Days of Supply dropped back to 48 on February 1, 2024 (Strong Seller’s Market).

Here is what we know from the fluctuations in Days of Supply and Home Price Appreciation when the metric hits highs & lows:

When Days of Supply reaches the 90 range, we see home prices softening (falling in some cases). And, when the Days of Supply falls well below the 60 mark, we observe home prices increasing. When Days of Supply was between 18 and 40, we saw double digit home price appreciation, multiple offers, and homes being bid up well above asking prices.

None of us has a crystal ball, and Days of Supply varies in both price segments and within neighborhoods for a variety of reasons. The ability of your Realtor to do an ongoing analysis of Days of Supply in your neighborhood should be a very strong consideration in who you select to market your home.

Knowing which way the market is trending while selecting a list price or reviewing offers is essential for home sellers looking to maximize their equity.

If you are having thoughts about selling your home or investment property, I can be reached at 714-336-0394

It is one of very few units with an oversize front window offering an abundance of light. The unique location offers views of the deepwater in the front rooms, and lagoon view from the kitchen, dining room, living room, patio, and master suite.

This home was completely remodeled and now features an “open floor plan” that spans the entire first floor. New kitchen cabinets, giant kitchen island, granite slab counters, stainless appliances, travertine flooring, dual pane windows, step down living room with warm fireplace. Additional upgrades include: Recessed lights, custom rod iron banister, wood floors in upper hall and secondary bedrooms.

The primary bedroom has an amazing view that must be seen, multiple closets, and remodeled bath. The powder room & hall bath are also remodeled. Additional conveniences include upstairs laundry and 2 car private garage.

The Seagate community has a spacious clubhouse, tennis & pickle ball courts, pool, spa, and many social opportunities including a yacht club. Buying in Seagate offers the opportunity to join the Huntington Harbour lifestyle where the climate is wonderful and all the recreational activities you enjoy are right out the front door:

Surfing, kite boarding, beach fun, bike riding, strolls on the sand, golf, parks, and schools are all nearby… Other unique activities in the area include paddle boarding, kayaking, fishing, and boating.

There is a Boat Slip are available to rent if you purchase this townhouse… ask for details!

Friends and family are eager to visit homeowners in Huntington Harbour and Huntington Beach to watch the holiday boat parade, 4th of July Parade/Fireworks, Pacific Air Show, and US Open of Surfing!

This home has one of the most relaxing and quiet locations in the area, yet it is just a short drive to Harbour View Elementary School, restaurants & shopping at the Harbour Mall.

If you ride your bike down Warner Avenue to Bolsa Chica Beach, it is possible to ride along the sand all the way to Newport Beach!

For more information, contact the listing agent for 16123 Saint Croix, Huntington Beach, CA: Scot Campbell 714-336-0394

This Modern Luxury Quality Home + Guest House was just completed and it is ideal for a multi-generational household or for owners who like to entertain out of town guests comfortably for extended time periods!

It is nestled in a very quiet neighborhood of custom homes on oversize homesites.

The main house is 4 Bedrooms, 4.5 Baths (4626 SqFt) and the Guest House (Legal ADU) is 2 Bedrooms, 2.5 Baths (1001 SqFt).

The house & ADU have separate meters for all utilities and there is a four car garage and 3 car driveway.

The design, finishes, and ambiance is impossible to describe… this property must be experienced “in person”.

Come join the Huntington Beach lifestyle where the climate is wonderful and all the recreational activities you enjoy are right out the front door:

Surfing, kite boarding, beach fun, bike riding, strolls on the sand, golf, parks, and schools are all nearby.

Just a few blocks away is Huntington Harbour which offers paddle boarding, kayaking, and marinas to keep your yacht or rent a Duffy boat for a harbour cruise.

Friends and family are eager to visit homeowners in Huntington Beach to watch the 4th of July Parade/Fireworks, Pacific Air Show, and US Open of Surfing!

This home has one of the most relaxing and quiet locations in the area, yet it is just a short stroll to Harbour View Elementary School, restaurants & shopping at the Harbour Mall.

If you ride your bike down Warner Avenue to Bolsa Chica Beach, it is possible to ride along the sand all the way to Newport Beach! The Home Automation system built into this home offers convenience and livability that you will truely enjoy. Come take a look before it is sold!

This is your opportunity to join the “Coastal Lifestyle” in comfort and style in this gorgeous 3 Story Modern style beach home!

It was Expertly Designed and Built in 2019 by a developer who was able to maximize the living area, balcony, and deck space in a way never previously approved by the planning department.

This is a remarkable home, it has no upper level set backs. The architect skillfully obtained planning department approval of the revolutionary design… there is more living area and deck space than any of the other New Homes recently built in the area. There is “more to love” about this house… definitely worth a look!

Located on one of the quietest blocks in Downtown HB (almost no traffic), yet just a short stroll to Parks, Pacific City, Main Street Village, and the soft sands of Huntington Beach! This home is in “like new” condition, and features: 3 Bedrooms + Office + Bonus Room | 4.5 BATHS | Open Floorplan | Huge Front Patio with BBQ & Linear Fire Pit | Approximately 3341 SqFt of living area | Oversize Lot | Air Conditioning | Elevator | Gourmet Island Kitchen with Breakfast Bar | Gorgeous Artistic Wine Cellar | Dramatic Floating Staircases & So much more!

This Open Concept Great Room Design features gourmet island kitchen with breakfast bar, professional quality appliances, dining areas, artistic wine cellar wall, powder room, and attached two car garage on the first level. The large front patio was designed for hosting parties.

The second floor features an office/family room, luxury master suite, and another in-suite bedroom with large private balcony.

The 3rd Floor is like none of the other homes developers build in the area. The top floor is like a Guest House featuring: a bedroom with full bath & private balcony, sitting area, living area with another full bath & walk-in closet, and finally another large deck with outdoor fireplace and BBQ area! Your family & guests will appreciate your hospitality, and of course all three levels are serviced by an elevator for convenience.

Arguably the best combination of design, location, and luxury features & upgrades to be found in Downtown Huntington Beach. And, the Price per Square Foot is the best you will find for a Recently Constructed home in the area… this home is a fantastic design & value!

Source: California Assn of Realtors – by Huntington Beach Realtor Scot Campbell – 714-336-0394

As always, there are many new laws going into effect for the New Year. There are some that homeowners and landlords should be aware of.

Below is a summary of laws going into effect in 2024:

GENERAL HOUSING LAW CHANGE:

Increases the exemption limit for improvements otherwise subject to the California Coastal Act

The California Coastal Act previously exempted improvements of $25,000 or less if necessary to protect life and public property from imminent danger.

This exemption limit is now increased to $125,000 which amount will be adjusted annually for inflation pursuant to the consumer price index.

The California Coastal Act of 1976 (Coastal Act) requires those wishing to facilitate development within the coastal zone to obtain a permit from both the California Coastal Commission and the local government. Previously, the Coastal Act exempted improvements necessary to protect life and public property from imminent danger from seeking a permit if the improvements are valued under $25,000. AB 584 increases this exemption to $125,000 and permits that amount to be adjusted annually for inflation pursuant to the consumer price index. C.A.R. supported AB 584, which facilitates improvements necessary to protect life and property from loss resulting from natural weather events through a reasonable increase in the Coastal Act’s permit exemption cap. This law seeks to assist coastal landowners in their efforts to protect their homes in an economy experiencing rising costs due to rising interest rates and materials costs.

Assembly Bill 584 is codified as Public Resources Code § 30611. Effective January 1, 2024

LANDLORD / TENANT LAW CHANGE:

Security deposits limited to one month’s rent.

Landlords may collect no more than one month’s rent for either furnished or unfurnished units in addition to first month’s rent.

There is an exception (two months rent allowed) for small landlords, defined as a landlord who is a natural person or LLC and owns no more than two residential rental properties with no more than a total of four units offered for rent.

AB 12, beginning July 1, 2024, prohibits a landlord from demanding or receiving security for a rental agreement for residential property in an amount or value in excess of an amount equal to one month’s rent, regardless of whether the residential property is unfurnished or furnished, in addition to any rent for the first month paid on or before initial occupancy.

Exception for small landlords: A small landlord may demand or receive a deposit in an amount or value not in excess of 2 months’ rent, whether or not the unit is furnished, in addition to any rent for the first month, if the landlord (1) is a natural person or a limited liability corporation in which all members are natural persons and (2) owns no more than 2 residential rental properties that collectively include no more than 4 dwelling units offered for rent. The exception for small landlords includes family trusts.

This small landlord exception does not apply if the prospective tenant is a service member.

Landlords who currently hold a security deposit or demand or collect a security deposit in excess of one month’s rent prior to July 1, 2024, may continue to retain the security even if it is more than one month’s rent.

Assembly Bill 12 is codified as Civil Code 1950.5. Effective July 1, 2024.

LANDLORD / TENANT LAW CHANGE:

Landlord must offer “ability to pay” in lieu of reliance on credit history and reports in assessing a tenant’s rental application when prospective tenant is receiving a government rent subsidy such as a Section 8 rental voucher

Landlord must offer “ability to pay” in lieu of reliance on credit history and reports in assessing a tenant’s rental application when prospective tenant is receiving a government rent subsidy such as a Section 8 rental voucher.

SB 267 makes it unlawful, in instances where there is a government rent subsidy, for a landlord to use a person’s credit history as part of the application process for a rental accommodation without offering the applicant the option, at the applicant’s discretion, of providing lawful, verifiable alternative evidence of reasonable ability to pay the portion of the rent to be paid by the tenant, including, but not limited to, government benefit payments, pay records, and bank statements.

When so offered, the applicant may elect to provide alternative evidence of reasonable ability to pay.

In which case the landlord must:

Provide the applicant reasonable time to respond with that alternative evidence and

Reasonably consider that alternative evidence in lieu of the person’s credit history in determining whether to offer the rental accommodation to the applicant.

Nonetheless, the landlord may still request information or documentation to verify employment, to request landlord references, or to verify the identity of a person.

Senate Bill 267 is codified as Government Code § 12955. Effective January 1, 2024.

LANDLORD / TENANT LAW CHANGE:

Tenant Protection Act: Tightens up requirements for no fault evictions; adds damages, penalties, attorney fees and enforcement mechanisms for violations.

This law tightens up the requirements for a landlord to terminate a tenancy under the Tenant Protection Act (i.e., California statewide rent cap and just cause eviction law) for no-fault evictions based upon owner move-in or substantial remodeling.

Additionally, an owner who violates the TPA by improperly terminating a tenancy or by raising rent beyond the maximum amount is liable for actual damages, reasonable attorney’s fees and costs (at the discretion of the judge), up to three times actual damages for willful violations and punitive damages. The Attorney General et al is authorized to seek injunctive relief. Effective April 1, 2024.

Background: The Tenant Protection Act of 2019 is a statewide rent cap and just cause eviction law. Under the TPA, there are only four permissible reasons on which a landlord may base a no-fault termination of tenancy. Senate Bill 567 seeks to close perceived loopholes in two of them: terminations based on owner-move and those based on demolishing or substantial remodeling. SB 567 also seeks to address the question of remedies for a violation of the TPA. Currently, the TPA does not specify damages or enforcement mechanisms.

Termination of tenancy based on owner move-in:

Under SB 567 in order to lawfully evict a tenant for just cause on the basis of an owner move-in:

The owner must identify in the written eviction notice the name and relationship to the owner of the intended occupant and include notification that the tenant may request proof that the intended occupant is actually an owner or related to the owner.

The owner or their family member would have to move in within 90 days after the tenant vacates and then occupy the unit for at least one year

The owner or their family member could not already occupy a unit and there could not be another vacant unit at the property.

If the intended occupant does not actually move in within 90 days or use the unit as their primary residence for at least a year, the owner must offer the unit back to the tenant who was evicted at the same rent and lease terms in effect at the time they vacated and reimburse the tenant for reasonable moving expenses incurred in excess of the required relocation assistance payment that may have been made in connection with the eviction.

If the former tenant does not move back in, and the owner subsequently identifies a new tenant still within the yearlong period after the eviction, the unit must continue to be offered at the lawful rent in effect at the time the eviction occurred and

The owner has to be a natural person holding at least a 25% ownership interest in the property (in order to prevent someone who holds a very small share of the property from evicting a tenant), a natural person who co-owns the property entirely with family members either outright or via a family trust, or a natural person who meets the 25% ownership threshold and whose recorded interest in the property is owned through an LLC or partnership.

Termination based on intent to demolish or to substantially remodel the residential real property:

Remodeling must require the tenant to vacate for 30 Consecutive Days. The remodel must not be able to be reasonably accomplished in a safe manner that allows the tenant to remain living in the place and must require the tenant to vacate the property for at least 30 consecutive days.

However, the tenant is not required to vacate the property on any days where a tenant could continue living in the property without violating health, safety, and habitability codes and laws.

Written Notice. A written notice terminating a tenancy must include all of the following:

A statement informing tenants of the intent to demolish or substantially remodel the unit, The following statement verbatim:

“If the substantial remodel of your unit or demolition of the property as described in this notice of termination is not commenced or completed, the owner must offer you the opportunity to re-rent your unit with a rental agreement containing the same terms as your most recent rental agreement with the owner at the rental rate that was in effect at the time you vacated. You must notify the owner within 30 days of receipt of the offer to re-rent of your acceptance or rejection of the offer, and, if accepted, you must reoccupy the unit within 30 days of notifying the owner of your acceptance of the offer”,

A description of the substantial remodel to be completed, the approximate expected duration of the substantial remodel, or, if the property is to be demolished, the expected date by which the property will be demolished,

A copy of the permit or permits required to undertake the substantial remodel. However, if the renovation is to abate hazardous materials then no permit need be given unless legally required.

A notification that if the tenant is interested in reoccupying the rental unit following the substantial remodel, the tenant must inform the owner of their interest and provide to the owner their address, telephone number, and email address.

SB 567 further provides that any termination notice that does not comply with any provision of the just cause rules is void.

Damages and enforcement mechanisms: Recovery of possession

An owner who attempts to recover possession of a rental unit in material violation of the just cause provisions will be liable for:

Actual damages.

In the court’s discretion, reasonable attorney’s fees and costs.

Upon a showing that the owner has acted willfully or with oppression, fraud, or malice, up to three times the actual damages. An award may also be entered for punitive damages for the benefit of the tenant against the owner.

The Attorney General et al is authorized to seek injunctive relief based on violations of the just cause rules.

Damages and enforcement mechanisms: Collecting or demanding rent beyond the maximum.

An owner who demands, accepts, receives, or retains any payment of rent in excess of the maximum rent shall be liable in a civil action for all of the following:

Injunctive relief.

Damages in the amount by which any payment demanded, accepted, received, or retained exceeds the maximum allowable rent.

In the court’s discretion, reasonable attorney’s fees and costs.

Upon a showing that the owner has acted willfully or with oppression, fraud, or malice, damages up to three times the amount by which any payment demanded, accepted, received, or retained exceeds the maximum allowable rent.

The Attorney General et al is authorized to 1)Enforce the provisions of this section and 2)Seek injunctive relief based on violations of this section.

Note on “actual damages” for material violation in termination of tenancy rules:

A tenant who has been wrongfully evicted is now authorized to recover actual damages. How might one calculate actual damages? The case of DeLisi v Lam, (2019) 39 Cal.App.5th 663, which involved the San Francisco rent control ordinance, is illustrative of how open ended the calculation can be. In the DeLisi case, the judge permitted the jury to weigh two competing (and mutually exclusive) methods of determining actual damages, as set forth by the expert witnesses for each side.

First, according to the expert for the tenant, actual damages are the difference between the rent being paid by the tenant and the market rate rent, multiplied by the tenant’s intended length of occupancy. The tenant testified that she intended to stay five or ten years. Under the San Francisco ordinance, a triple damage penalty is automatically applied. Taking into account the present value of a ten-year tenancy, the expert arrived at a figure of $287,180. That figure multiplied by three would allow for total damages of approximately $860,000.

The expert for the landlord took a different view. In his view, the value of the rent-controlled tenancy was not an asset the tenant could monetize. Instead, damages would be the amount the tenant was out-of-pocket beyond what she would have been if she had stayed in the rent-controlled apartment. This included moving expenses, the difference between her monthly rent at the rent-controlled property and her monthly rent at her new apartment, and any differences in expenses for items such as commuting to work. All in all, “actual damages” would be $23,139 for a five-year period and $48,183 for a 10-year period. Multiplied by three these dollar figures are still considerable, but a far cry from amount calculated by the tenant’s expert.

The jury returned a verdict for $120,000 which multiplied by three equals $360,000. Which theory of “actual damages” did the jury base their decision on? No one knows for sure. Juries are not required to report the basis of their decisions. (They can be asked to answer specified questions. But even there, they are not reporting the reasoning behind their decision).

Mind you, in many legal cases the attorney fees are staggering, often in excess of the actual damages awarded. Under SB 567 attorney fees may be awarded to the tenant at the discretion of the judge.

Senate Bill 567 is codified as Civil Code §§ 1946.2 and 1947.12.

Effective April 1, 2024.

LANDLORD / TENANT LAW CHANGE:

Tenants may keep bicycles, e-bikes and other “micromobility” transport devices in their units.

SB 712 prohibits a landlord from prohibiting a tenant from owning personal micromobility devices or from storing and recharging up to one personal micromobility device in their dwelling unit for each person occupying the unit, subject to certain conditions and exceptions.

Personal micromobility devices are things like bicycles, scooters, hoverboards, skateboards, and their electric counterparts such as an e-bike or e-scooter.

SB 712 prevents landlords from prohibiting tenants from owning personal micromobility devices and also prevents landlords from banning the storage and recharging of personal micromobility devices in their dwelling units if the devices meet certain criteria as follows:

either,

They are not powered by an electric motor, or

They comply with certain safety standards for e-bikes and e-scooters (see below), or

Failing compliance with such safety standards, the tenant has insurance covering storage of the device within the unit.

Batteries for e-bikes should comply with either the UL 2849 standard, recognized by the United States Consumer Product Safety Commission, or the EN 15194 European Standard for electrically powered assisted cycles. E-scooters, on the other hand, need to align with the UL 2272 standard from the U.S. or the EN 17128 European Standard for personal light-electric vehicles.

However, landlords have the option to provide tenants with exterior “secure, long-term storage” for their devices. If such storage is offered without charge, landlords can prohibit the in-unit storage of these devices.

A landlord is not required to modify or approve a tenant’s request to modify a rental dwelling unit for the purpose of storing a micromobility device inside of the dwelling unit. A landlord may prohibit repair or maintenance on batteries and motors of personal micromobility devices within a dwelling unit. A landlord can require a tenant to store a personal micromobility device in compliance with applicable fire code.

Question: Can the landlord prohibit a tenant from storing a bike on the balcony?

A: Unclear. A landlord cannot prohibit a tenant from storing a device “in their dwelling unit.”

Senate Bill 712 is codified as Civil Code 1940.41. Effective January 1, 2024.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

May 12, 2024 | 714-336-0394 | Scot@CampbellRealtors.com | Broker of Record – Coldwell Banker-Campbell Realtors

May 12, 2024 | 714-336-0394 | Scot@CampbellRealtors.com | Broker of Record – Coldwell Banker-Campbell Realtors

16123 Saint Croix is a stunning waterfront townhome on the Lagoon in the Seagate community in Huntington Harbour.

16123 Saint Croix is a stunning waterfront townhome on the Lagoon in the Seagate community in Huntington Harbour. The primary bedroom has an amazing view that must be seen, multiple closets, and remodeled bath. The powder room & hall bath are also remodeled. Additional conveniences include upstairs laundry and 2 car private garage.

The primary bedroom has an amazing view that must be seen, multiple closets, and remodeled bath. The powder room & hall bath are also remodeled. Additional conveniences include upstairs laundry and 2 car private garage. There is a Boat Slip are available to rent if you purchase this townhouse… ask for details!

There is a Boat Slip are available to rent if you purchase this townhouse… ask for details!

Come join the Huntington Beach lifestyle where the climate is wonderful and all the recreational activities you enjoy are right out the front door:

Come join the Huntington Beach lifestyle where the climate is wonderful and all the recreational activities you enjoy are right out the front door: This home has one of the most relaxing and quiet locations in the area, yet it is just a short stroll to Harbour View Elementary School, restaurants & shopping at the Harbour Mall.

This home has one of the most relaxing and quiet locations in the area, yet it is just a short stroll to Harbour View Elementary School, restaurants & shopping at the Harbour Mall. Questions?

Questions?

A unique home is available for purchase in Downtown Huntington Beach!

A unique home is available for purchase in Downtown Huntington Beach! This Open Concept Great Room Design features gourmet island kitchen with breakfast bar, professional quality appliances, dining areas, artistic wine cellar wall, powder room, and attached two car garage on the first level. The large front patio was designed for hosting parties.

This Open Concept Great Room Design features gourmet island kitchen with breakfast bar, professional quality appliances, dining areas, artistic wine cellar wall, powder room, and attached two car garage on the first level. The large front patio was designed for hosting parties. Arguably the best combination of design, location, and luxury features & upgrades to be found in Downtown Huntington Beach. And, the Price per Square Foot is the best you will find for a Recently Constructed home in the area… this home is a fantastic design & value!

Arguably the best combination of design, location, and luxury features & upgrades to be found in Downtown Huntington Beach. And, the Price per Square Foot is the best you will find for a Recently Constructed home in the area… this home is a fantastic design & value!